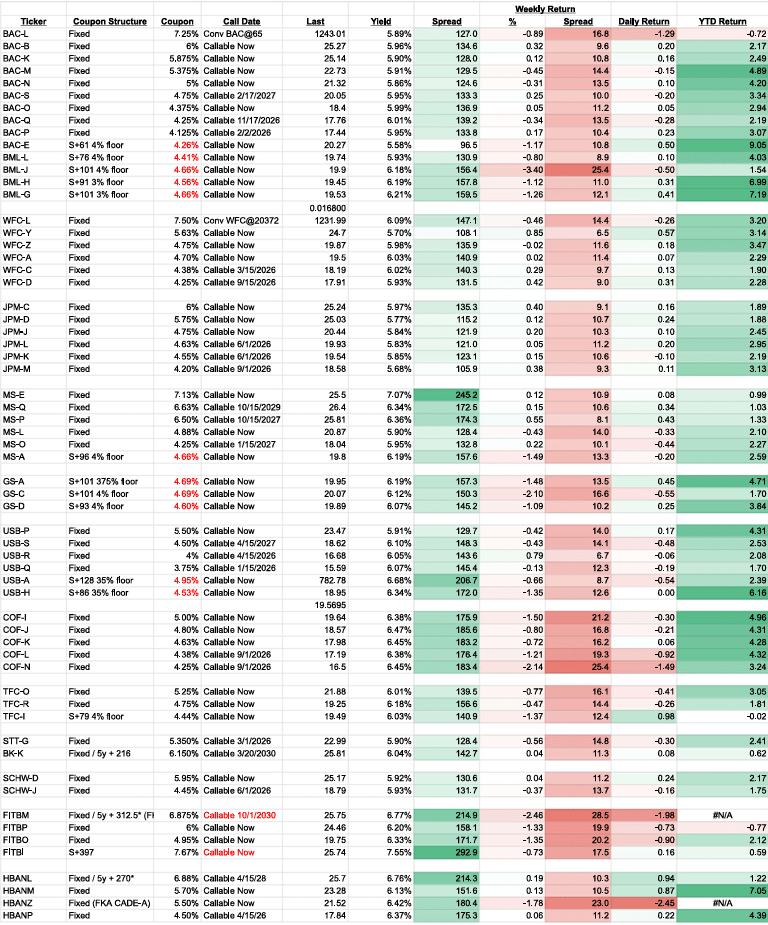

Fixed rate pref yields were relatively stable for the week despite treasury yields falling 10-15 bps (treasury yields fell, especially on Friday on renewed private credit fears. Thus spreads widened 10-15bps across most fixed rate issues (more in some cases for COF and FITB).

COF and FITB widened the most (~15bps or more) during the week vs 30y treasuries in part due to their common stock underperforming. Out of all issuers, JPM performed best.

Floaters had a second straight week of underperformance. BAC and USB Floaters still remain relatively attractive vs fixed rate despite floaters outperforming thus far on the year (see dashboard below).

Source: Google Finance and Atticus Research calculations. Note, floating rate prefs are assumed to be swapped into a fixed rate (30y treasury less 72bps reflecting the negative swap spread). Spreads are vs 30y treasury yields.

Leave a comment